by Koh Teng Teng

Share

Share

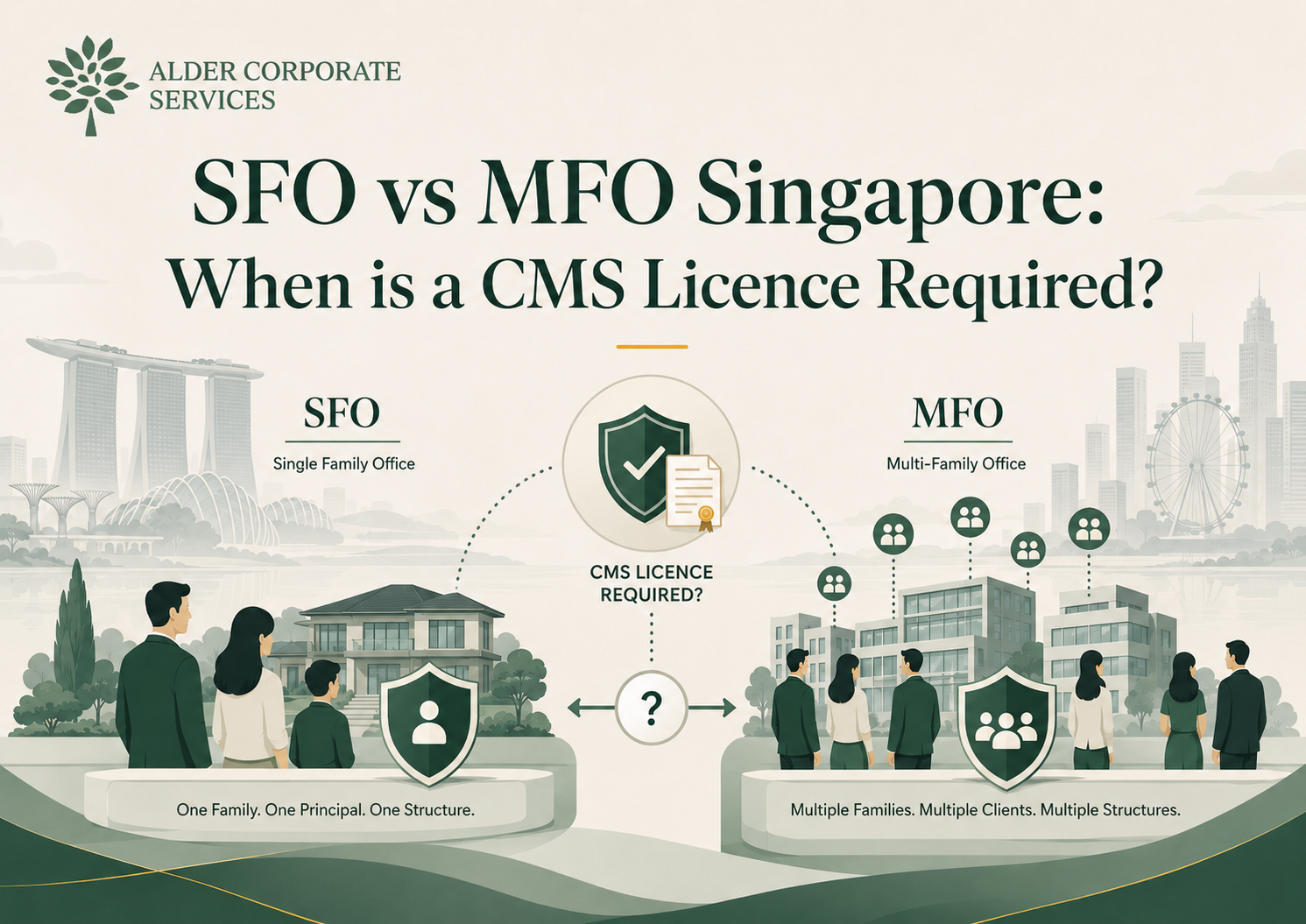

SFO vs MFO in Singapore: When Does a Family Office Need a CMS licence?

This article is written for fund managers, investment professionals and family office founders considering structure and licensing decisions in Singapore. It focuses on the regulatory line between a Single Family Office (SFO) and a Multi‑Family Office (MFO) and the practical triggers that make a Capital Markets Services (CMS) licence necessary—rather than acting as a general relocation or lifestyle guide.

Singapore’s family office ecosystem has expanded rapidly in recent years and benefits from policy support such as tax incentives (including Section 13O/13U) and clear AML frameworks. Those incentives and the available onshore fund structures make the city attractive, but qualifying for tax or operational incentives does not automatically mean a family office is exempt from licencing—the activities a firm undertakes determine whether it is genuinely an SFO or has crossed into regulated fund management.

Alder assists fund managers and family office platforms in assessing the appropriate licensing route before engaging MAS.

What is a Single Family Office (SFO)?

Single family office (SFO) — in regulatory terms — is an entity that manages the assets and financial affairs of one family group only, typically through a private company or trust that is wholly owned and controlled by family members. The core compliance question for founders and investment professionals is straightforward: does the office manage only related‑party family assets, or does it provide fund management services to unrelated clients?

For licensing purposes, the formality of the structure (Pte Ltd, trust, VCC) is secondary to the activities conducted. An SFO that simply consolidates and manages family capital, accepts no third‑party money, does not market investment services, and does not operate pooled vehicles is more likely to be treated as a non‑regulated SFO — subject, however, to AML/CFT, PDPA and any reporting tied to tax incentives.

Source: VCC

Practical SFO example (compliance focus): A family hires two investment professionals to manage only family‑owned assets held in a Singapore private company. The office takes no management fees from unrelated parties, does not market services, and does not operate pooled vehicles — likely an SFO for MAS purposes, though AML/CFT and reporting requirements remain.

Key red flags that can push an SFO towards licencing risk: accepting third‑party capital, charging management or performance fees to non‑family clients, offering discretionary mandates to unrelated investors, marketing investment services in Singapore, or creating pooled VCC sub‑funds that admit non‑family investors. If any of these occur, the entity should promptly assess whether it has become a fund manager under the SFA.

If your SFO sits close to these red lines, Alder can help assess whether to rely on the SFO exemption, appoint a CMS‑licensed outsourced manager, or apply for a CMS licence.

What is a Multi‑Family Office (MFO)?

MFO describes a professional investment and wealth management platform that manages assets for more than one unrelated family. The defining point from a regulatory perspective is client base and activity: once a platform manages portfolios for multiple unrelated families — particularly on a discretionary basis, charges fees to clients, operates pooled vehicles, or markets services in Singapore — it increasingly looks like regulated fund management rather than a private family office.

In Singapore, firms operating as MFOs commonly operate under licensed fund management entities or appoint a Singapore‑based CMS licence holder to manage the investment function. This is because MFO activity often involves pooled structures (for example VCC sub‑funds), admission of non‑family investors, and provider fees — all activities that sit squarely within the Securities and Futures Act definitions of fund management unless a clear exemption applies.

For founders and investment professionals weighing options, the practical paths are: (a) build an MFO and apply for a CMS licence; (b) appoint an outsourced, MAS‑licensed fund manager to handle regulated activities and compliance; or (c) restructure operations to remain a private SFO — for example by avoiding third‑party capital, not marketing services and limiting activity to related parties. Alder can assess which route best suits your commercial model and regulatory position.

| Decision driver | Typical SFO (licence-exempt) | Typical MFO / Licensed manager (CMS likely required) |

|---|---|---|

| Client base | Single related family / related entities only | Two or more unrelated families, external investors or third-party clients |

| Fees & revenue model | Funded by family capital; typically no external management or performance fees charged to unrelated parties | Charges management and/or performance fees to clients; fee income from unrelated investors is common |

| Discretionary mandates | May be internal to family but limited to related parties | Common – discretionary portfolio management across multiple client accounts; regulatory trigger for CMS licensing |

| Pooled vehicles / fund structures | Typically none; family assets held in separate family entities, though VCCs can be used for internal structuring | Often operates pooled funds or VCC sub-funds that admit non-family investors – a strong indicator that a CMS licence is needed |

| Marketing / client solicitation | No marketing of investment services to public or unrelated parties | May market services or solicit clients – clear indicator of commercial fund management activity |

| AUM & tax incentives | SFOs can apply for tax incentives such as Section 13O / 13U, subject to AUM and spending criteria — but tax status is separate from licensing; verify thresholds with MAS/IRAS | MFOs operating pooled funds will typically need a CMS licence regardless of tax incentive status; AUM thresholds for different schemes, such as 13O and 13U, should be checked for eligibility |

| Compliance & reporting | Subject to AML/CFT, PDPA and MAS/IRAS annual declarations if receiving tax incentives | Full CMS licence compliance: AML/CFT, regular regulatory filings, audits, and obligations under the SFA |

Note: numerical thresholds for tax incentive eligibility (for example under Section 13O/13U) and Employment Pass or local spend requirements change over time — verify current AUM and spending criteria with MAS/IRAS when making structural decisions.

Next step: if the facts on your structure point toward multiple unrelated clients, fee income, pooled vehicles, discretionary mandates or active marketing, you should treat the arrangement as potential fund management and assess CMS licencing. Alder can help you review the facts, determine whether an exemption is sustainable, or prepare an application for a CMS licence — see Alder’s MAS licensing support: Alder — MAS licensing support.

Family office regulatory framework

Regulation of family offices in Singapore sits with the Monetary Authority of Singapore (MAS). The regulatory test is activity‑based: MAS distinguishes single family offices (SFOs) from multi‑family or client‑facing businesses primarily by what the entity does and to whom it provides services, not by branding or marketing labels.

Single‑Family Offices (SFOs)

SFOs that manage assets exclusively for one family and its related entities are generally treated differently from commercial fund managers. MAS has moved from ad‑hoc, case‑by‑case exemptions toward a class exemption framework for genuine SFOs — the aim is to provide clarity on when a family office may be licence‑exempt while ensuring appropriate safeguards for AML/CFT and investor protection.

Under the class exemption approach (see MAS consultation response), SFOs seeking to rely on an exemption typically need to demonstrate that they:

- Are wholly owned and controlled by members of the same family

- Are incorporated or effectively established in Singapore

- Maintain a business relationship with a MAS‑regulated financial institution (for AML/CFT linkage and banking/custody)

- Have at least one Singapore‑resident liaison or employee to engage with MAS where needed

Important: meeting these criteria helps with exemption eligibility but does not remove other regulatory responsibilities. Exempt SFOs remain subject to AML/CFT requirements, PDPA data protection rules, and any MAS/IRAS reporting tied to tax incentives (for example, schemes under Section 13O/13U). The existence of a tax incentive (13O/13U) is a separate test to the licence test — a tax‑efficient setup does not automatically mean an entity is licence‑exempt.

Multi‑Family Offices (MFOs) and licensed managers

Where an office provides investment management or discretionary services to two or more unrelated families, admits external investors, charges management or performance fees, operates pooled vehicles (for example VCC sub‑funds) or markets services in Singapore, MAS will typically consider the activity within the scope of regulated fund management. Such businesses commonly require a Capital Markets Services (CMS) licence and must comply with the SFA, AML/CFT rules and ongoing reporting obligations.

For investment professionals and founders, the practical implication is that hiring non‑family investment staff, setting up pooled funds, or moving to a fee‑based model can change your regulatory classification. Where there is doubt, an early assessment is prudent: either to document an SFO‑only model that remains within exemption boundaries, appoint an outsourced MAS‑licensed manager, or begin a CMS licence application.

MAS consultation response and guidance (November 2024) provide more detail on the class exemption framework — check MAS for the latest position and transitional arrangements.

MAS consultation response (Nov 2024)

When an SFO may remain licence‑exempt — a practical compliance checklist

- Single‑family control — the entity is wholly owned and controlled by members of the same family and manages only related‑party assets.

- No external clients or third‑party capital — the office does not accept monies from unrelated investors, friends, business partners or other families.

- No pooled funds for outsiders — the office does not operate pooled vehicles or VCC sub‑funds that admit non‑family investors.

- No marketing or solicitation — it does not market investment management services or solicit clients in Singapore.

- No fee‑for‑service model to unrelated parties — it is funded by family capital rather than charging management/performance fees to third parties.

- Operational footprint consistent with exemption — local staffing, banking relationship and governance are aligned with MAS requirements for SFOs (liaison presence, AML linkage, record keeping).

Clear red flags that trigger a CMS licence assessment: accepting co‑investors or third‑party money; onboarding unrelated families as ongoing clients; charging management or performance fees to outside investors; giving discretionary mandates over third‑party portfolios; creating or managing pooled fund structures; or actively marketing investment services in Singapore. Any of these will usually move the activity into the scope of regulated fund management.

Note that an SFO reliant on tax incentives (for example under Section 13O) must still meet reporting and local spend/AUM requirements — tax status is distinct from the licensing test. If you are evaluating whether your arrangement remains a private single family vehicle or has crossed into fund management, an early, fact‑based review is recommended.

If the arrangement sits between private family management and client‑facing fund activity, Alder can assess whether an exemption, an outsourced CMS‑licenced manager, or a direct CMS licence application is the appropriate route.

When a CMS licence should be considered

If a family office moves beyond managing only related‑party capital, it commonly falls within the scope of regulated fund management. MAS expects entities that conduct regulated activities under the Securities and Futures Act to hold the appropriate authorisations — typically a Capital Markets Services (CMS) licence. Below are the practical scenarios that should prompt a CMS licence assessment.

- Managing assets for more than one unrelated family — ongoing investment management for unrelated clients is a primary trigger.

- Accepting external investors or third‑party client money — any admission of non‑family capital usually takes the activity outside SFO exemptions.

- Charging management or performance fees to clients — a commercial, fee‑based model points to regulated fund management.

- Discretionary authority over investment portfolios — making investment decisions on behalf of unrelated clients is a common licensing trigger.

- Marketing investment management services in Singapore — active solicitation or public facing offers increases licensing risk.

- Operating pooled funds, sub‑funds or VCC strategies for multiple families — pooled legal structures that admit non‑family investors will generally require a licensed fund manager.

- Holding out as a fund manager, wealth manager or investment manager — representations to counterparties or investors that you are providing professional management can be decisive.

- Not clearly falling within an available exemption — if facts and commercial terms are ambiguous, treat the arrangement as potentially regulated and seek an assessment.

For practical guidance on the licensing steps and MAS expectations, see the MAS CMS licence guidance: CMS licence Singapore — MAS guidance.

If you’re unsure whether your platform needs a CMS licence, Alder can help review your facts, advise on licence versus exemption, or prepare a CMS licence application: Alder — MAS licensing support.

Common licensing triggers — quick checklist for fund managers and family office founders

Use this checklist to decide whether your family office activity is likely to require a CMS licence or other regulated authorisations. Any one of the following is a meaningful trigger to conduct a licensing assessment:

- Manages assets for more than one unrelated family — ongoing management of unrelated clients usually converts a private office into a fund management activity.

- Accepts external investors or third‑party client money — admitting non‑family capital is a common regulatory watershed.

- Charges management or performance fees to clients — a commercial fee model indicates fund management rather than purely internal family servicing.

- Has discretionary authority over portfolios — acting on behalf of unrelated investors is typically within the SFA scope.

- Markets investment management services in Singapore — solicitation or public offers materially increase licensing risk.

- Operates a pooled fund, sub‑fund, or VCC strategy for multiple families — pooled structures that admit outsiders generally require a licensed manager.

- Holds itself out as a fund manager, wealth manager or investment manager — representations to investors/counterparties can determine regulatory classification.

- Does not clearly fall within an available exemption — where facts are ambiguous, treat the arrangement as potentially regulated and seek professional advice.

Source: VCC

If any of these triggers apply to your platform, undertake an early licencing assessment — either to confirm an available exemption, to appoint an outsourced MAS‑licensed manager, or to prepare a CMS licence application. For MAS guidance on licensing, see: MAS — CMS licence. Alder can assist with a fact‑based review and licensing application support: Alder — MAS licensing support.

Practical examples: when an SFO stays private and when licencing is required

The following concise vignettes illustrate common fact patterns and the likely MAS implication. Each example ends with a recommended next step for fund managers, investment professionals or family office founders.

Example 1 — Pure SFO (likely licence‑exempt)

Facts: A family sets up a Singapore private company to hold and manage only family assets. Two investment professionals (one non‑family) report to the family CFO. No management fees are charged to outsiders; no pooled vehicles are offered and there is no marketing.

MAS implication: Activity aligns with a traditional SFO. The office should document ownership, client scope and controls to support exemption reliance and meet AML/CFT and reporting obligations (including any Section 13O/13U filings if incentives are claimed).

Next step: Compile a factual memorandum demonstrating single‑family control and no third‑party activity; verify tax incentive requirements if applying under Section 13O.

Example 2 — Platform for unrelated families (licence likely required)

Facts: A former private banker launches a management platform and signs on three unrelated families as ongoing clients, charges management fees and has discretion over portfolio implementation.

MAS implication: Managing unrelated client money on a discretionary and fee‑forming basis is a primary trigger for CMS licensing under the SFA.

Next step: Stop and conduct a licensing assessment immediately. Options include (i) applying for a CMS licence, or (ii) appointing an outsourced MAS‑licensed fund manager to perform regulated activities while the platform remains an advisory/ops hub.

Example 3 — Co‑investment and ‘friends’ joining a vehicle (fast trigger)

Facts: An SFO offers co‑investment opportunities and admits friends, business partners and a small number of external investors into a special vehicle for certain deals.

MAS implication: Even limited third‑party admission can negate exemption — accepting third‑party capital or creating pooled vehicles is commonly treated as fund management.

Next step: Pause onboarding of non‑family investors and seek immediate regulatory advice. Consider using an outsourced licensed manager or redesigning co‑investments as bespoke arrangements that avoid pooled fund mechanics.

Example 4 — VCC sub‑funds with non‑family investors (clear licensing need)

Facts: A family office uses a VCC umbrella and creates sub‑funds that admit non‑family investors or pooled capital from multiple families.

MAS implication: VCC sub‑funds with external investors require a MAS‑licensed fund manager; the VCC structure does not remove the need for a CMS licence where regulated activities are conducted.

Next step: Prepare for CMS licence engagement or contract a licensed manager to operate the fund management function and handle fund administration/AUM reporting.

Across all examples, document the factual matrix (who are the clients, where funds originate, what discretion exists, whether fees are charged, the legal vehicle used). That factual record is the primary input for an MAS licensing decision or for structuring a defensible SFO exemption.

How Alder can assist

If your organisation is a family office or fund platform and you are weighing SFO vs MFO choices, Alder provides practical, compliance‑first support tailored for fund managers, investment professionals and family office founders. Our services focus on the licensing decision and on keeping structures aligned with MAS expectations.

- Licensing assessment: a fact‑based review to determine whether your activities trigger CMS licensing, or whether an SFO exemption is sustainable.

- CMS licence application support: end‑to‑end assistance preparing application materials, compliance manuals and regulatory submissions for MAS.

- Exemption and restructure advice: practical options to avoid unnecessary licencing where appropriate (e.g., appointing an outsourced MAS‑licensed manager, redesigning co‑investment mechanics).

- Compliance framework design: AML/CFT, KYC/KYSOW, PDPA and reporting processes tuned to MAS and IRAS obligations, including documentation for Section 13O/13U tax incentive applications when relevant.

- Operational readiness: governance, controls and vendor selection (fund administrator, custodian, auditors) to meet licence or exemption requirements.

If your model sits between a private single family vehicle and a client‑facing fund business, an early assessment reduces regulatory risk and execution delays. For MAS guidance on the CMS licence application, see: MAS — CMS licence.

To discuss a licensing assessment or CMS licence application, contact Alder’s MAS licensing team: Alder — MAS licensing support.

Final note: tax incentives such as Section 13O/13U and any S$50 million thresholds are relevant commercial considerations, but they do not substitute for a licensing test — structure and activity drive whether a CMS licence or an exemption applies.

About the Author: Koh Teng Teng

For years, many financial institutions (FIs) in Singapore treated their Anti-Money Laundering and Countering the Financing of Terrorism (AML/CFT) frameworks as a “set and forget” exercise. As long as the Enterprise-Wide Risk Assessment (EWRA) was updated annually and names were run through a screening database, compliance officers felt secure. However, the mid-2025 amendments to MAS